Help Wanted: Government Statisticians

I asked AI what the market thinks about the June BLS jobs report and here’s what it told me: “Goldilocks” for stocks, dovish for the Fed, bullish for bonds — but with some labor-market yellow flags. Translation: a weak number is good for the stock market and bonds. NOT! Both were down on the day. Interest rates have marched higher while the equity market is flat since the report.

The stock market initially rallied because a weak jobs number means that the Fed won’t be mean and raise rates. Whether the Fed raises rates or not has little to do with jobs and more to do with our $40t in debt, $2t annual budget deficit and the $10t in new treasury issuance required over the next year. In other words, the bond market will set the rate (at least at the long end).

Back to the jobs report. The unemployment rate fell to 4.2 percent because 720,000 citizens allegedly stopped looking for jobs. If that sounds strange, it is.

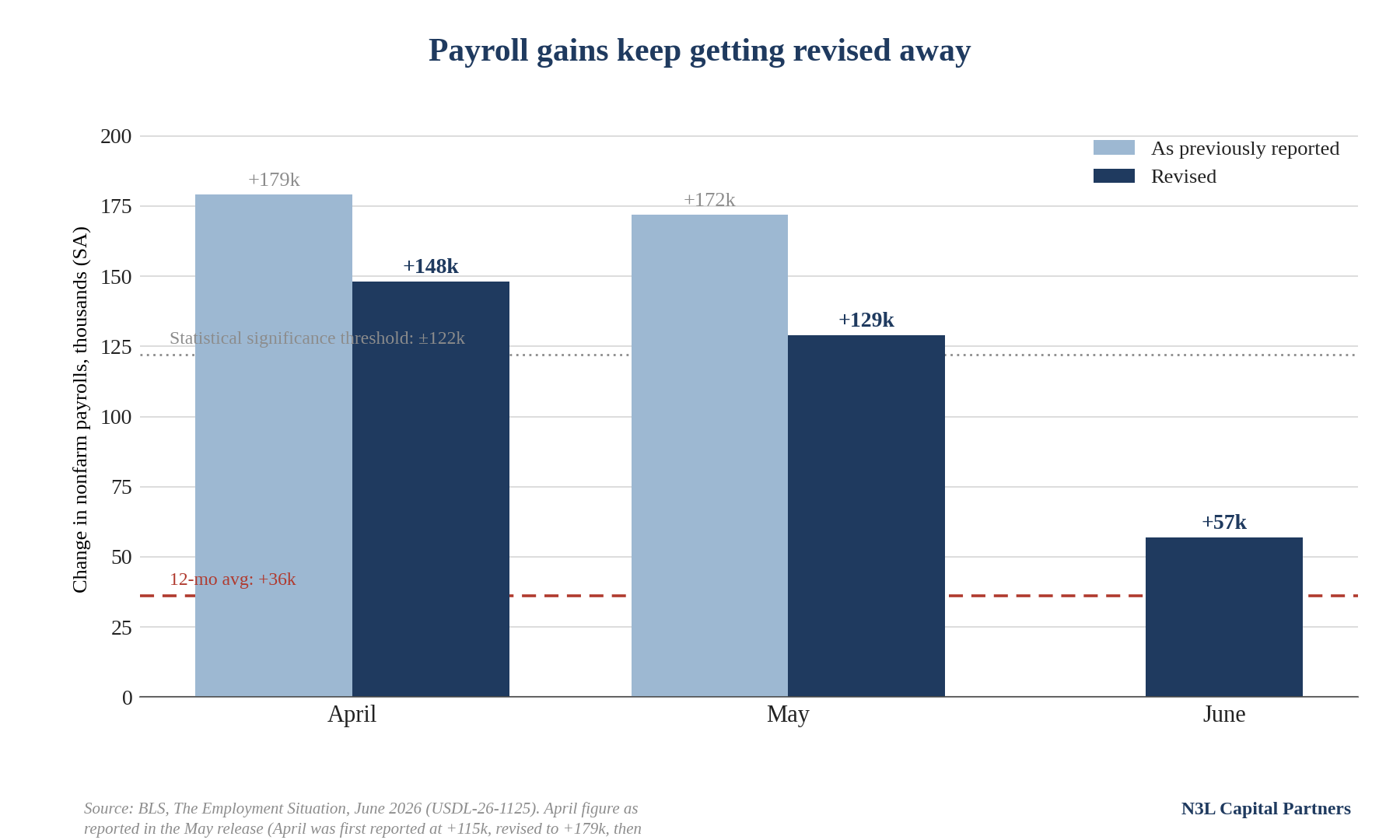

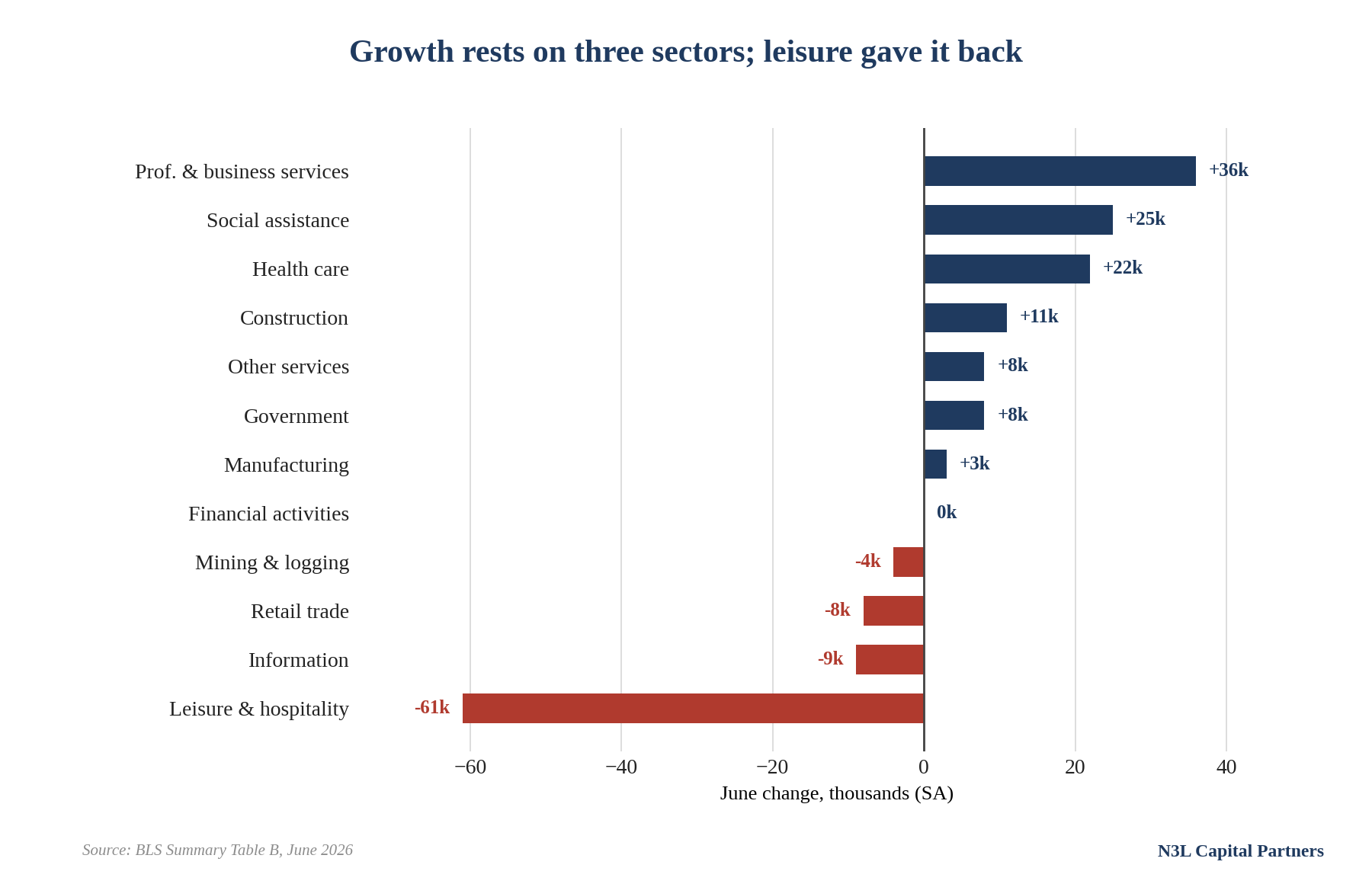

Of the 57,000 jobs added, 47,000 of them were in health care and social assistance - quasi government jobs. Restaurants and hotels cut nearly 55,000 jobs in June; the month they're supposed to be hiring everyone with a pulse. And past reports were revised down. In April and May, we were told that 74,000 jobs were created that simply weren’t.

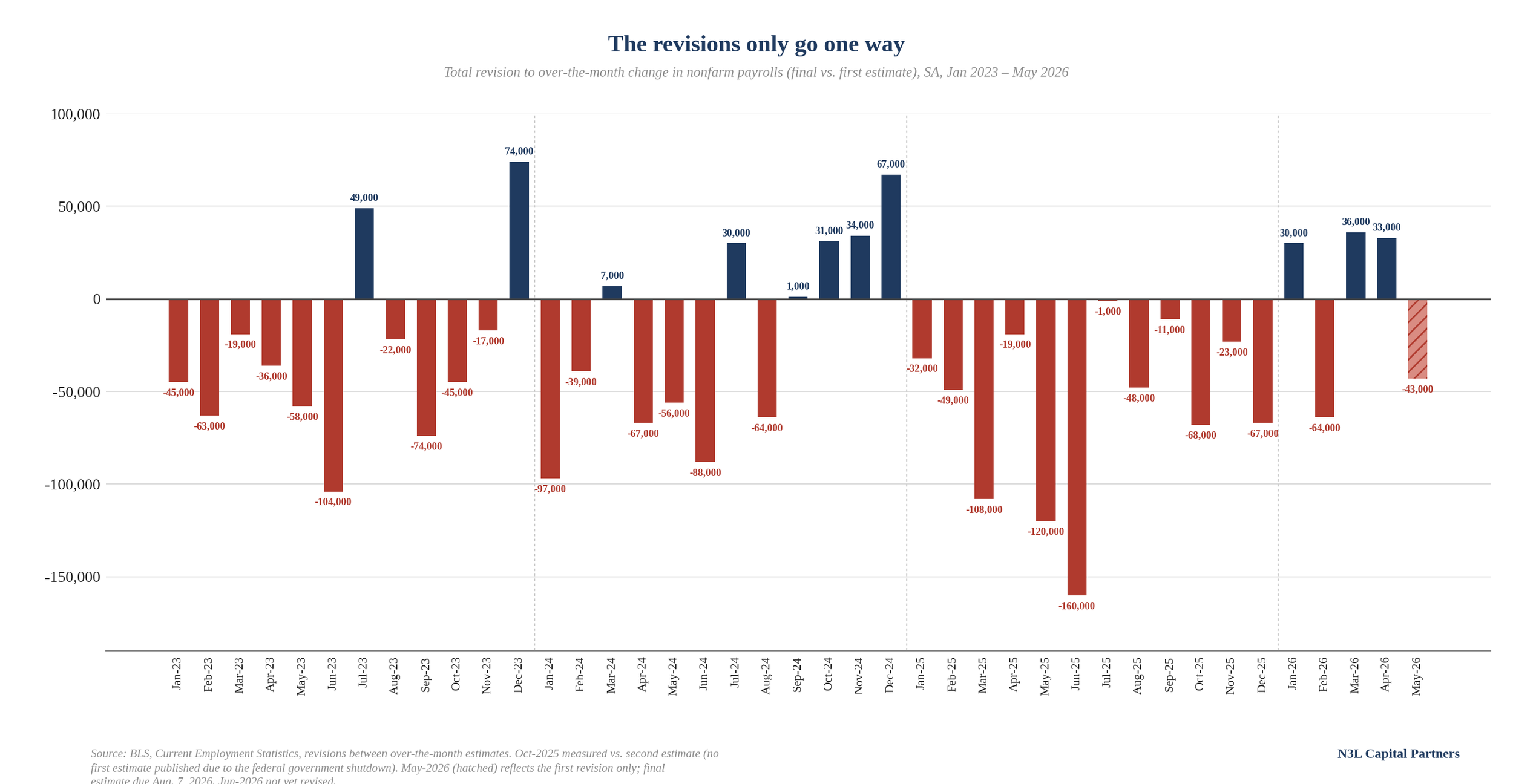

This isn't just a three-month problem. Over the past three and a half years, the BLS has revised its own numbers down post the official report in 30 out of 41 months. In 2025, every single month was revised lower by a total of 700,000 jobs. Remember when Trump barked that the downward revisions were politically motivated and he demanded a new head of the BLS? Well, we have a new (interim) head of the BLS and nothing has improved.

Why the Jobs Report is Weak

Breadth is the core problem. Health care and social assistance (~+47,000 combined) plus professional and business services (+36,000) account for more than the entire net gain. Strip them out and the rest of the private economy lost jobs in June. The private diffusion index sits at 54.4, barely above the 50 line that separates expansion from contraction, meaning nearly half of all industries are cutting. Health care itself is decelerating: its 22,000 June gain is well below its 38,000 twelve-month average. The labor market's last reliable engine is downshifting.

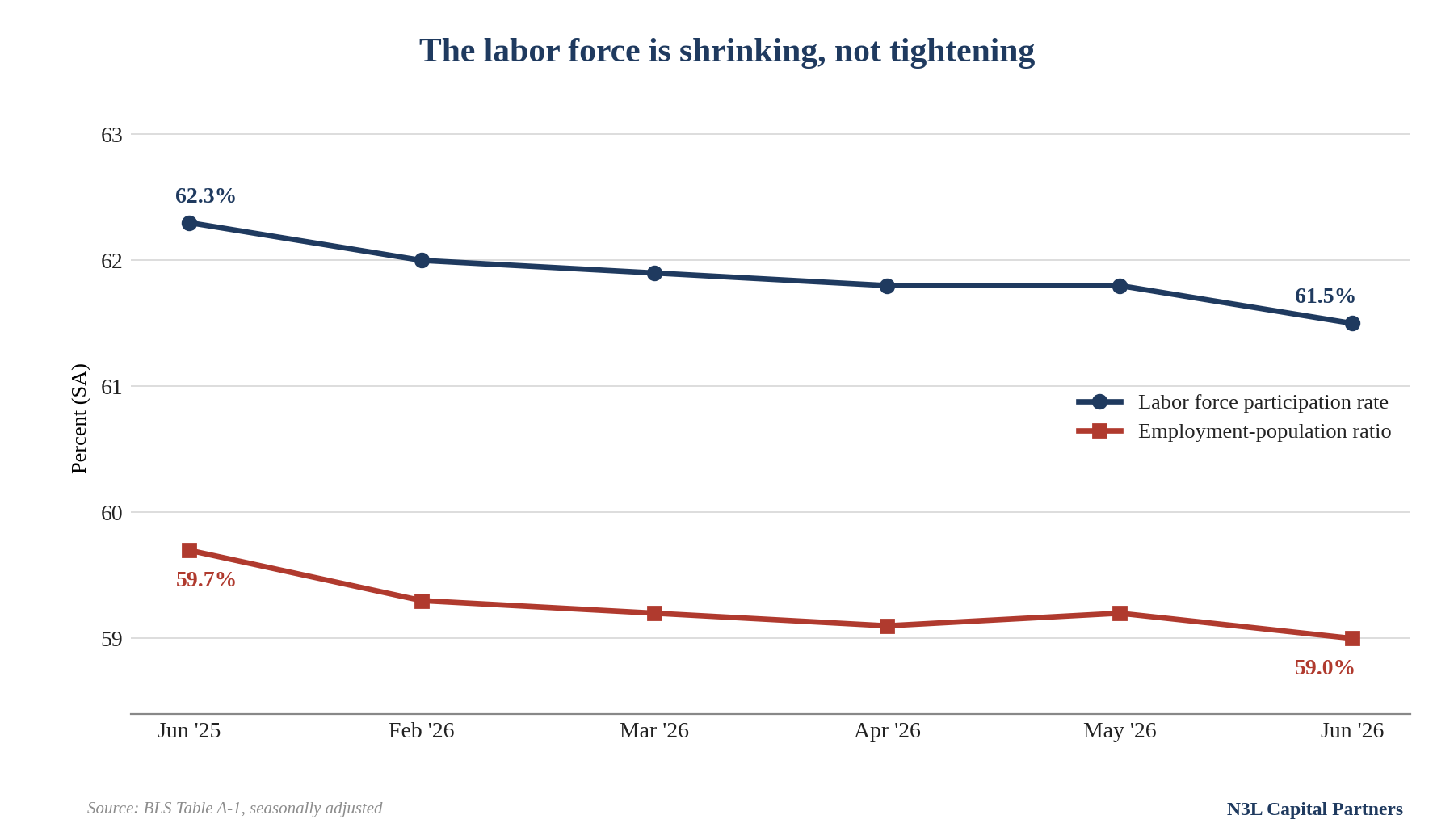

Wait…only 59% of the population is even working (see below)! Who’s going to pay the taxes to support the massive growing U.S. debt and deficits? Maybe the robots that are supposed to replace the rest of us…

Unless otherwise noted, information included herein is presented as of the dates indicated. N3L Capital Partners (together with its affiliates, "N3L") makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the information contained herein, including, but not limited to, information obtained from third parties or government sources, including the U.S. Bureau of Labor Statistics, which is subject to revision by the source agency. Opinions, estimates and projections constitute the current judgment of the author as of the date indicated. They do not necessarily reflect the views and opinions of N3L and are subject to change at any time without notice. N3L does not have any responsibility to update the information to account for such changes. Hyperlinks to third-party websites in these materials are provided for reader convenience only. There can be no assurance that any trends discussed herein will continue. The information contained herein is not intended to provide and should not be relied upon for accounting, legal, or tax advice and does not constitute an investment recommendation or investment advice. Readers should make an independent investigation of the information contained herein, including consulting their tax, legal, accounting or other advisors about such information. N3L does not act for you and is not responsible for providing you with the protections afforded to its clients. N3L and its affiliates may hold positions in securities, instruments, or asset classes discussed herein.