Inflation Post Mortem

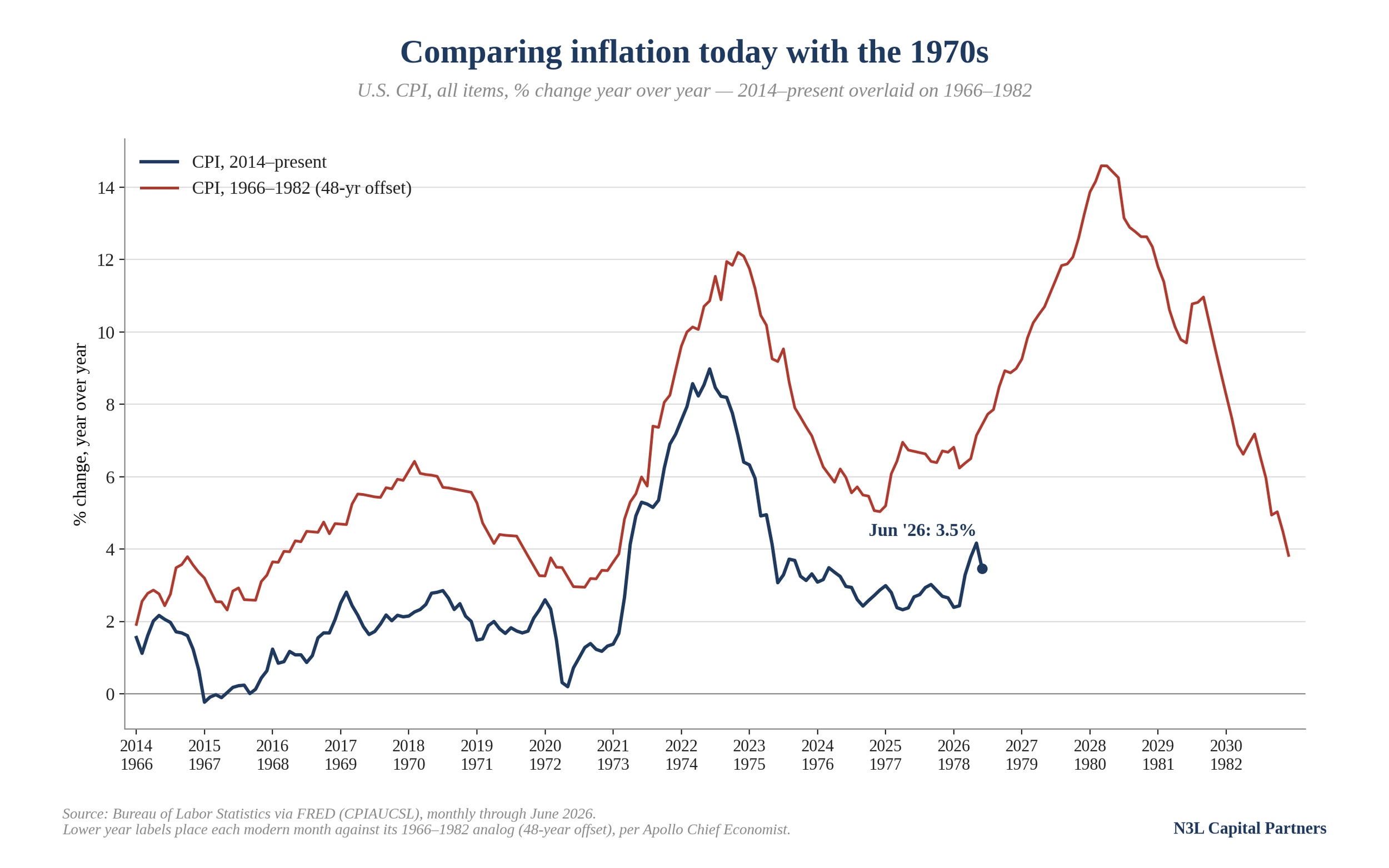

Yesterday’s “lower than expected” CPI of 3.5% made the monkeys and the machines excited. Today’s PPI headline on CNBC bragged that “Wholesale prices unexpectedly declined in June on a big drop in gasoline.”

I have two questions: How is it good news that prices rise only 3.5% per annum - at this pace, prices double in just 20 years - and why was it a shocker (to the experts) when oil and gas were the two categories that were “surprised” on the downside? Beware the headlines!

CPI and PCE are backward looking. Oil prices have risen 14% in less than a month since the last period as Iran calls Donald Trump’s bluff and his tweets aren’t enough to matter now that bombs are flying again. July’s CPI number will reverse to the upside and the headlines will bleat again. Ignore them. Inflation is a problem for the citizens, Kevin Warsh, Scott Bessent and the Republicans in the midterm elections. All of this was unnecessary. Tariffs, war and soaring government debt are all inflationary. There is an economics lesson here.

Trump the Stock Picker

It seems like Donald Trump is a better stock picker with his money than ours. Just a month and a half ago, he gave $1b of our money to IBM. Well, there is deflation after all: yesterday, IBM stock lost $68b in market cap because they missed analysts’ expectations. IBM is a relic of a company of course that sells mainframe computers and the software that runs them. If you haven’t heard, mainframes are dinosaurs.

Reminder: the government should not be picking winners and losers.

Unless otherwise noted, information included herein is presented as of the dates indicated. N3L Capital Partners (together with its affiliates, "N3L") makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the information contained herein, including, but not limited to, information obtained from third parties or government sources, including the U.S. Bureau of Labor Statistics, which is subject to revision by the source agency. Opinions, estimates and projections constitute the current judgment of the author as of the date indicated. They do not necessarily reflect the views and opinions of N3L and are subject to change at any time without notice. N3L does not have any responsibility to update the information to account for such changes. Hyperlinks to third-party websites in these materials are provided for reader convenience only. There can be no assurance that any trends discussed herein will continue. The information contained herein is not intended to provide and should not be relied upon for accounting, legal, or tax advice and does not constitute an investment recommendation or investment advice. Readers should make an independent investigation of the information contained herein, including consulting their tax, legal, accounting or other advisors about such information. N3L does not act for you and is not responsible for providing you with the protections afforded to its clients. N3L and its affiliates may hold positions in securities, instruments, or asset classes discussed herein.